Five Things to Know About The Economy

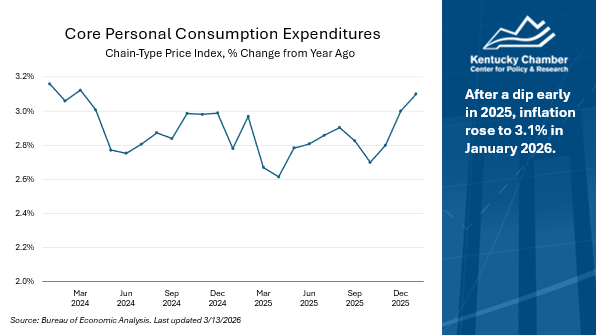

- Inflation: Inflation has been consistently higher than the Federal Reserve’s target rate of 2.0%, rising to 3.1% in January 2026.

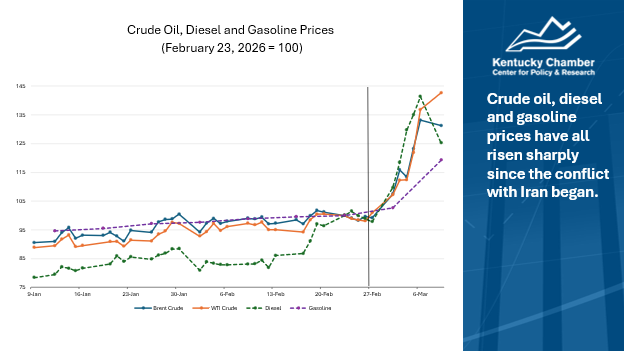

- Energy prices: Conflict in the Middle East has caused oil, diesel, and gasoline prices to spike. This has already affected the March Consumer Sentiment Survey and will affect other measures in the coming months. The longer the conflict continues, the more significant the effects on the economy will be.

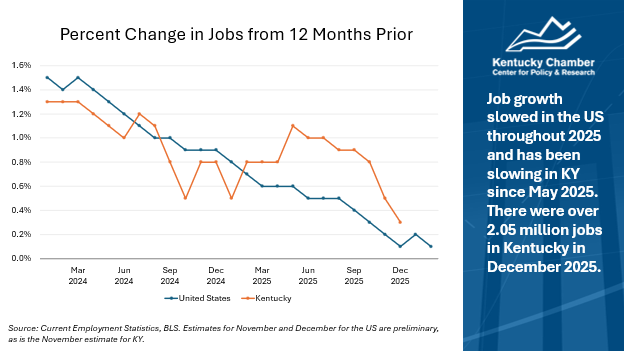

- Jobs and Employment: After poor job growth throughout 2025, the employment situation in January showed a glimmer of hope; however, the employment situation worsened in February with the U.S. losing 92,000 jobs. Job growth in Kentucky began following the weaker national trend in May 2025, as growth has slowed in the state.

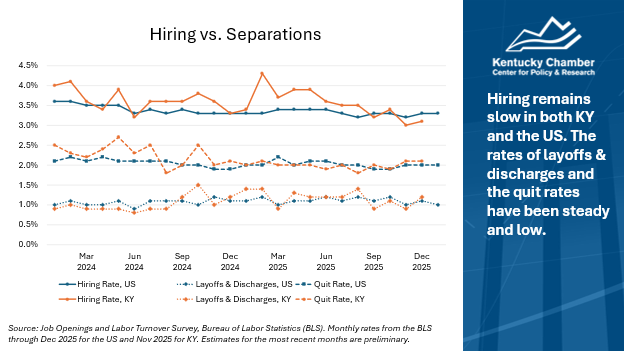

- Slow-hire, slow-fire: Firms appear less willing to hire, but also reluctant to make any major changes. Some call this a slow-hire/slow-fire labor market.

- GDP: GDP grew more slowly in 2025 (2.1%) than in 2024 (2.8%), consistent with the cooling labor market in 2025. GDP growth in Q4 2025 slowed to 0.7%.

Notes: This information is meant to provide a monthly check-in on the most recent economic data in Kentucky and the U.S. It is not comprehensive. For additional information on Kentucky’s economy, we recommend resources like Blueprint Kentucky’s annual report on Kentucky’s Rural Economy and the UK’s Annual Economic Report.

Here are more details on the state of the economy as of March 20, 2026.

Inflation

Inflation remains elevated above 3% and has risen over the past three months.

- Core PCE & the Fed: Core Personal Consumption Expenditures (PCE) – which excludes food and energy – is the Federal Reserve’s preferred inflation metric. The Fed targets 2% inflation using Core PCE, which the US has not seen since 2021.

- 2024 vs. 2025: Inflation in December 2025 was the same as in December 2024.

- 2025 vs. 2026: Inflation in January 2026 was higher than it was in January 2025.

- The Tariff Effect: The increase in inflation shown since April 2025 is consistent with the effects of tariffs.

- Iran's Impact on Inflation: The spike in energy prices due to war in the middle east will be felt by consumers and businesses more quickly than they show up in core inflation, which excludes food and energy prices.

Energy Prices

Energy prices rose sharply after the conflict with Iran began.

- Indexing Energy Prices: This chart indexes prices for diesel, gasoline, West Texas Intermediate Crude oil (the standard benchmark for U.S.-produced oil prices), and the internationally traded Brent Crude oil (the standard global benchmark) to February 23, 2026, just before the conflict with Iran started.

- Oil Prices: Both West Texas Intermediate Crude (WTI) and Brent Crude oil prices surged following the start of the conflict. In the first week of the conflict, WTI rose over 40%, and Brent Crude rose over 30%.

- Gasoline and Diesel Prices: According to the AAA website, the national average price for gasoline was $3.912 per gallon on March 20, 2026. The average price in Kentucky was $3.730, a 45% increase from the same period in February. The national average for diesel was $5.159, while it was $4.925 in Kentucky (also a 45% increase over the same time last month).

- Impacts: Diesel prices will have greater impacts on costs to businesses due to how they influence shipping expenses, while gasoline prices will disproportionately affect everyday households.

Job Growth

Job growth has slowed in both Kentucky and the U.S.

- How We Look at Jobs: This chart displays job growth by showing the 12-month change in jobs as a percentage, which allows for more direct comparisons between Kentucky and the U.S. and removes the seasonality of month-to-month changes.

- Slower Growth in the U.S.: Job growth slowed in the U.S. throughout 2024 and 2025, reaching almost 0% year-over-year growth by the end of last year. The U.S. added 181,000 jobs last year.

- 2026, So Far: January 2026 looked like a good month. The US added 126,000 jobs, with the health care sector accounting for most of that growth; however, the US lost 92,000 jobs in February. There was an unusual decrease of 28,000 health care jobs due to strike activity.

- Kentucky Job Growth: Kentucky saw positive changes in job growth in early 2025, but growth began slowing after May, and the state began following the national downward turn. Revisions to state-level job estimates are expected in April, which could change this picture (with the possibility of downward revisions to state numbers).

Hiring vs. Separations

Hiring is weak, but layoffs are mostly stable—creating a "slow-hire/slow-fire" dynamic.

- Slow Hire: Hiring in both Kentucky and the U.S. has deteriorated slowly. While the hiring rate in Kentucky was higher throughout much of 2025, it began falling in May 2025.

- Slow Fire: Layoffs and discharges held steady before increasing slightly with more recent months’ estimates. Firms appear less willing to hire, but also reluctant to make any major changes. Some call this a slow hire/slow fire labor market.

- Layoffs in the News: Media stories of mass layoff announcements usually provoke more concern than is warranted. BLS data suggest there are around 1.7 million layoffs and discharges every month in the US. That said, recent preliminary estimates show a small increase in layoffs.

- Slow Quit, Too: Quits have been low, suggesting workers aren’t finding (or expecting to find) better jobs than what they have.

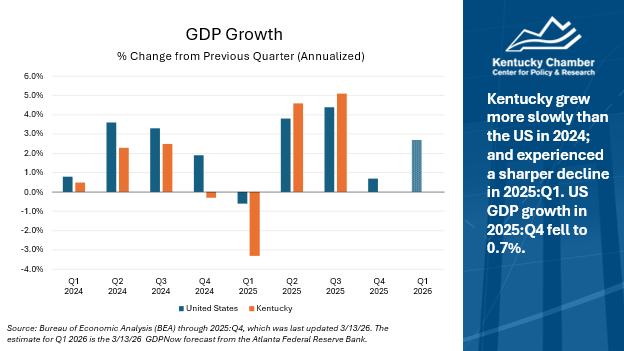

GDP Growth

National GDP growth slowed last year compared to 2024

- What GDP Is: Gross Domestic Product (GDP) = Consumption + Investment + Government spending + (Exports – Imports).

- 2025 vs. 2024: GDP grew more slowly in 2025 (2.1%) than in 2024 (2.8%).

- Q4 of 2025: The GDP growth in 2025:Q4 slowed relative to Q3 as government spending and net exports fell. Consumer spending slowed, and investment increased slightly

- Consumer Spending: GDP growth in 2025:Q3 was driven by increases in consumer spending, net exports, and government spending. The increase in consumer spending reflected increases in both goods and services. Among services, health care and “other services” were the leading contributors. Among goods, recreational goods, vehicles, and “other nondurable goods” (mainly prescription drugs) were leading contributors.

- Business Investments: A concerning detail about both the 2025:Q2 and Q3 increases is that they masked decreases in investment. These decreases are consistent with a cooling labor market despite GDP growth.

- Imports: The main driver of the decline in GDP in 2025:Q1 was a large increase in imports as firms pulled forward imports in anticipation of tariffs. The apparent rebound in 2025:Q2 was then associated with a decline in imports.

- Kentucky: The importance of manufacturing and wholesale trade to Kentucky likely explains why the changes in early 2025 were more pronounced for KY than for the US.

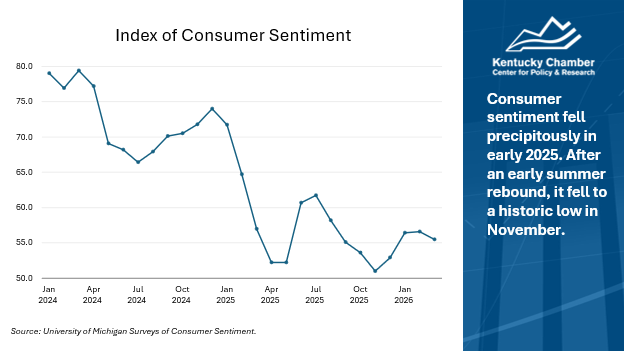

Consumer Sentiment

Consumer sentiment has improved since reaching at all-time low in November.

- Consumer Sentiment: The University of Michigan produces an index of consumer sentiment and updates it monthly.

- All-time Low Last November: The November 2025 reading of 51.0 was an all-time low on the index.

- March 2026 Lower Than March 2025: The preliminary estimate for March 2026, 55.5, is 2.7% lower than March 2025.

- Rebound Since November: Surveys of Consumers Director Joanne Hsu noted that the temporary increase in consumer sentiment in December 2025 and January 2026 was driven entirely by “consumers with the largest stock portfolios.” In early survey results from March, she added that the nine days of surveying since the beginning of the war in Iran reversed that improvement, with the increase in gas prices noted as having an impact.

About This Data

On this web page, we provide economic updates on Kentucky and the United States, using a range of key metrics from the U.S. Department of Labor, U.S. Bureau of Economic Analysis, the University of Michigan, the St. Louis Federal Reserve, and the U.S. Chamber of Commerce. All data is analyzed by the Kentucky Chamber Center for Policy and Research. On this page, we cover jobs, unemployment, unemployment insurance claims, hiring, workforce participation, inflation, consumer sentiment, and small business optimism.

Sources

Federal Reserve Bank of St. Louis, Federal Reserve Economic Data

MetLife and U.S. Chamber of Commerce, Small Business Index

University of Michigan, Survey Research Center, Surveys of Consumers

U.S. Bureau of Economic Analysis, Personal Consumption Expenditures Price Index

U.S. Bureau of Labor Statistics, Local Area Unemployment Statistics

U.S. Bureau of Labor Statistics, Labor Force Statistics from the Current Population Survey

U.S. Department of Labor, Employment and Training Administration, Unemployment Insurance Data

U.S. Federal Reserve, Economy at a Glance – Inflation (PCE)

ADP Employment Report

Carlyle

Revelio Labs

U.S. Tariffs on Track to Hit 84-Year High Under Current Proposals, Tax Foundation Says

The Kentucky Chamber hosted a webinar on June 9, 2025, featuring Vice President of Policy Charles Aull and Erica York, Vice President of Federal Tax Policy at the Tax Foundation, to explore how tariff and tax policies in Washington are shaping the economic landscape for Kentucky businesses.

Watch the webinar below: