What is the Kentucky Chamber's Economic Dashboard?

The Kentucky Chamber’s Economic Dashboard provides timely updates on economic conditions in Kentucky and across the United States. It tracks key indicators, including employment, workforce participation, hiring, inflation, consumer sentiment, and small business optimism, to help business leaders and policymakers understand current trends.

Current Economic Snapshot

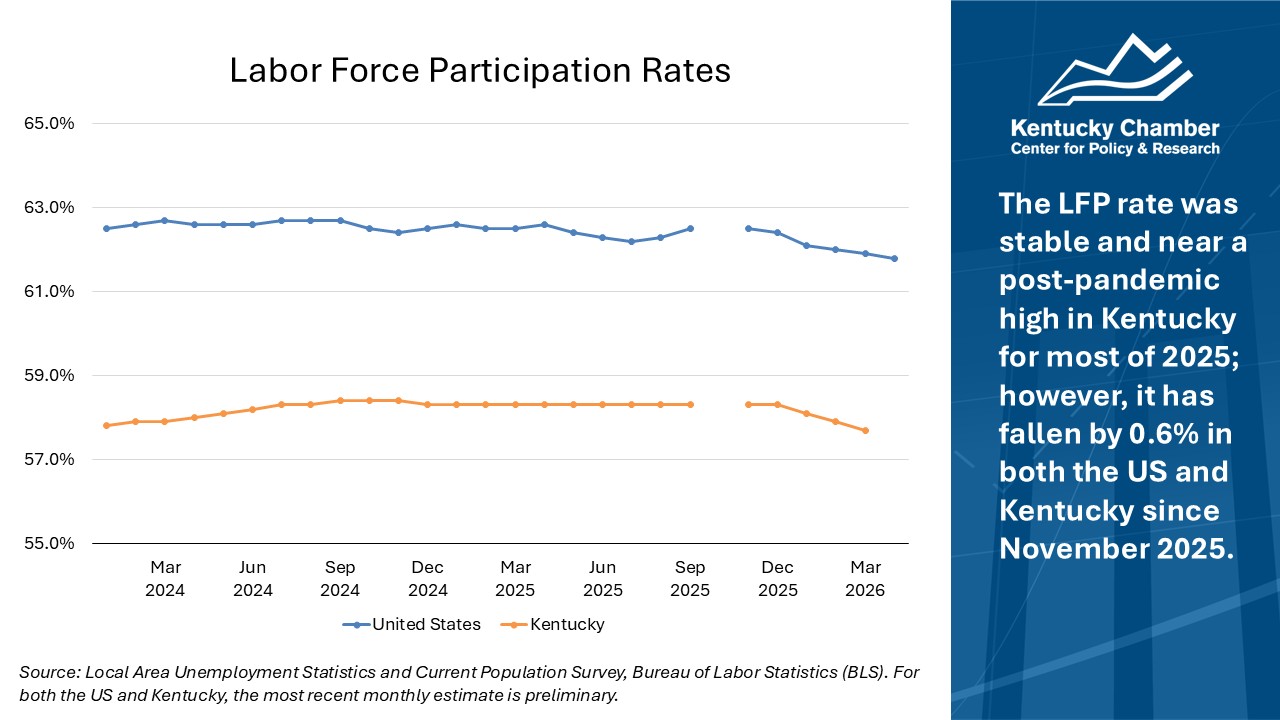

- Labor Force Participation: After a period of relative stability, labor force participation in Kentucky and the U.S. began falling in late 2025 and continued falling in the first quarter of 2026.

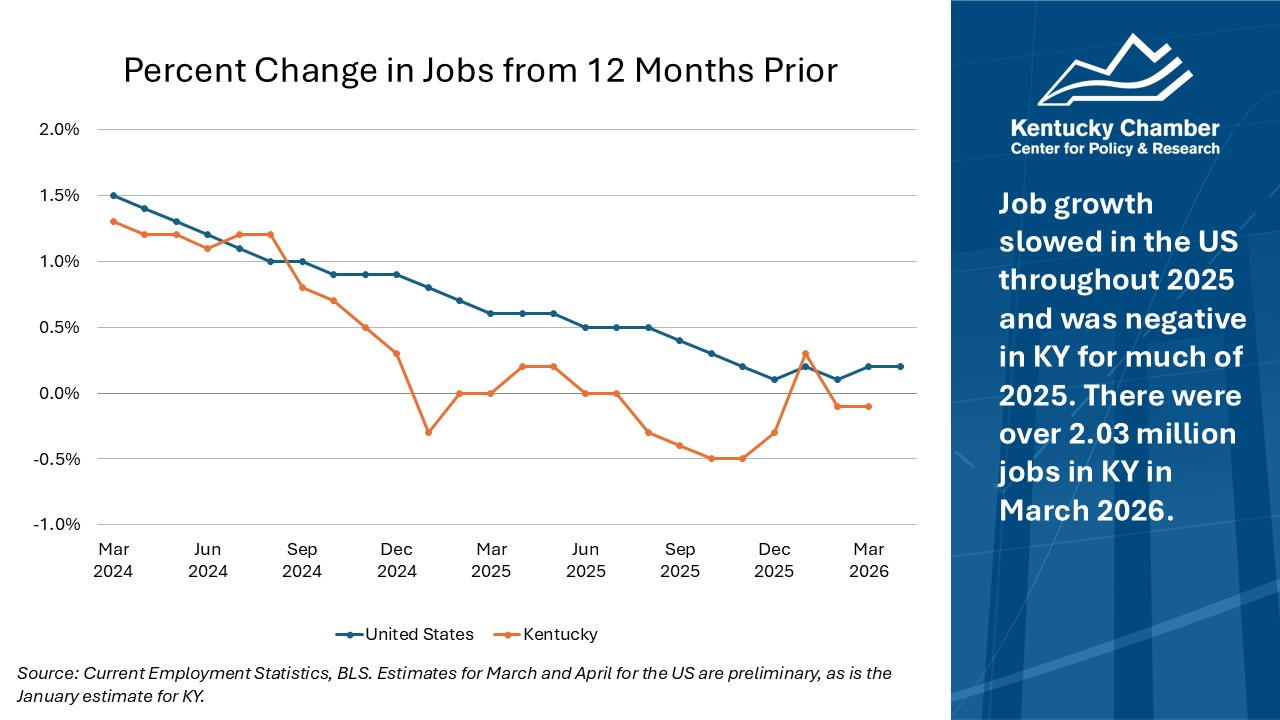

- Jobs: Job growth in Kentucky was negative for much of last year, according to newly revised data, while growth in the U.S. cooled considerably. 2026, so far, has been a mixed bag for jobs, with positive year-over-year growth in Kentucky in January but negative year-over-year growth in February and March.

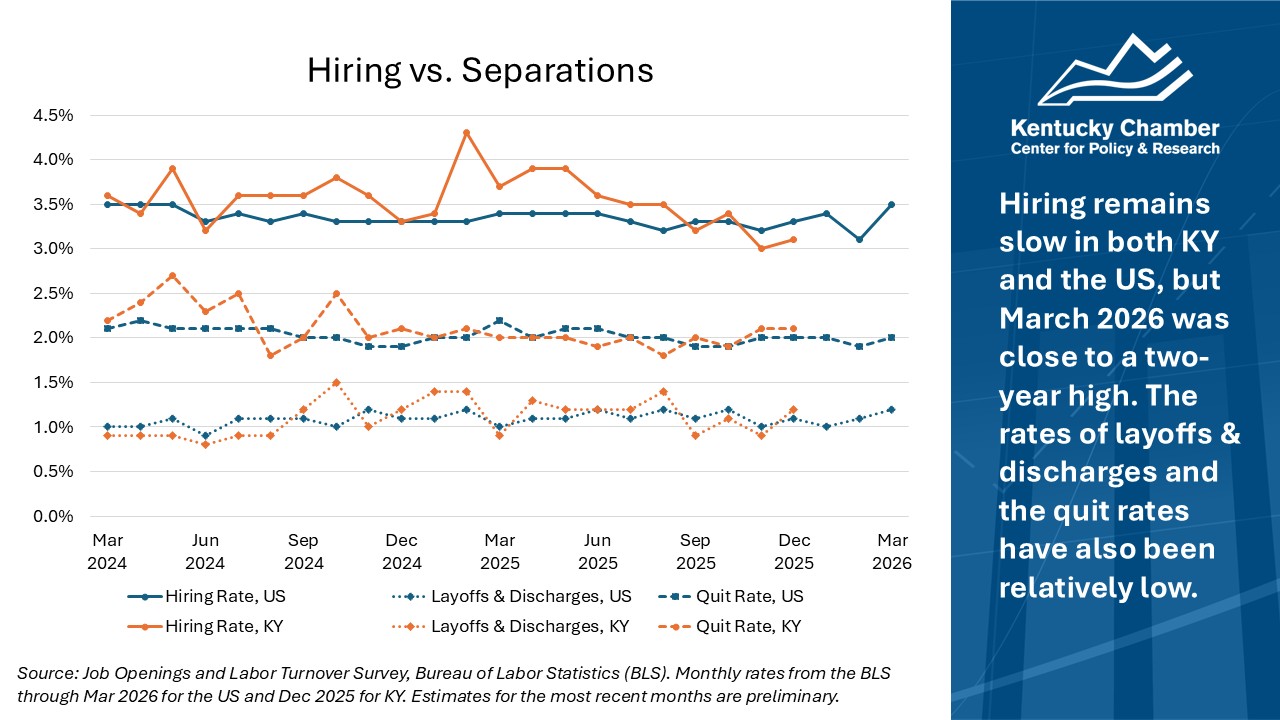

- Slow-hire, slow-fire: Businesses continue to appear less willing to hire, but also reluctant to make any major changes – like layoffs. This “slow-hire, slow-fire” job market, which characterized 2025, is extending into 2026.

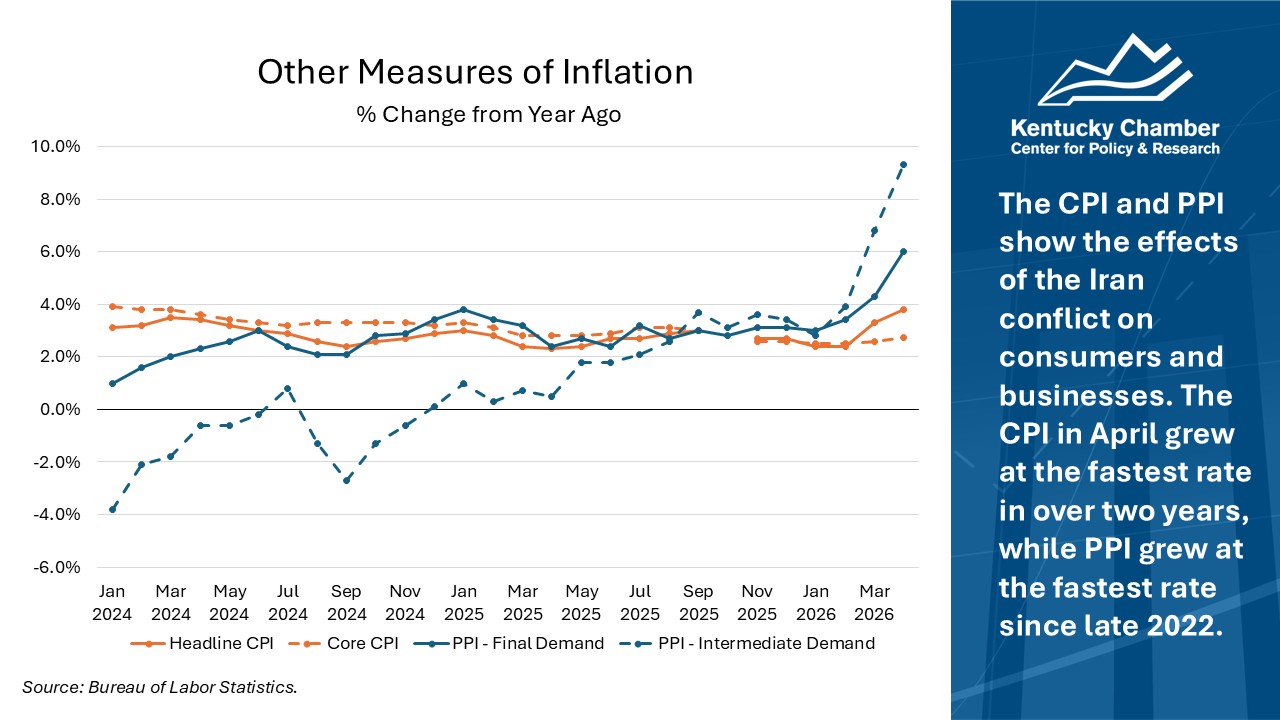

- Inflation: The Federal Reserve’s preferred measure of inflation continues to trend well above its target of 2 percent, while other measures of inflation indicate prices might soon rise even faster as uncertainty looms over the conflict in the Middle East.

- Energy prices: Conflict in the Middle East has caused oil, diesel, and gasoline prices to spike.

- Consumer sentiment: May marked a new all-time low for consumer sentiment, breaking a record set just last month, based on preliminary survey data.

Notes: This information is meant to provide a monthly check-in on the most recent economic data in Kentucky and the U.S. It is not comprehensive. For additional information on Kentucky’s economy, we recommend resources like Blueprint Kentucky’s annual report on Kentucky’s Rural Economy and the UK’s Annual Economic Report.

Here are more details on the state of the economy as of May 26, 2026.

Labor Force Participation

After a period of steadiness, labor force participation declined in 2026.

- Declining labor force participation. Labor force participation (the share of the 16+ population working or looking for work) was steady in the U.S. and Kentucky in 2025. From November 2025 to March 2026, however, the rate fell by 0.6% in both the U.S. and Kentucky.

- Fewer employed and unemployed adults. At the national and state level, the decline reflects a reduction in both employment and unemployment. Less employment accounted for approximately two-thirds of the decrease; however, considering that the unemployed accounted for at most 4.5% of the labor force in this period, a reduction in the number of unemployed played a proportionally large role.

- The gap between Kentucky and the U.S. Kentucky has historically trailed the nation in labor force participation rates. The causes of this gap are multifaceted, but the key drivers are low rates of educational attainment in Kentucky and a high share of the population living in rural areas. Kentucky’s urban areas have much higher rates of workforce participation than its rural areas, at 59.9% vs. 52.4%, respectively.

Job Growth

After a poor year for job growth, early 2026 shows signs of life in the labor market.

- Kentucky lost jobs last year: Kentucky ended 2025 with 5,700 fewer jobs compared to the same time in 2024, according to benchmark revisions released by the Bureau of Labor Statistics in April.

- Negative or flat growth in most months: In 2025, growth in 10 out of 12 months was either negative or flat for Kentucky. January 2026, however, saw a welcome uptick.

- National job growth slowed in 2025: The national picture for jobs was marginally better than in Kentucky, with the U.S. adding 181,000 jobs last year. But job growth cooled consistently throughout 2025.

- A mixed start to 2026: The U.S. added 160,000 jobs in January, with the health care sector accounting for most of that growth; lost 156,000 in February; gained 185,000 in March; and gained 115,000 in April. The average job growth so far in 2026 is 76,000 jobs per month. Job growth in April occurred mostly in health care, transportation and warehousing, and retail trade.

- How we look at jobs: The chart above displays job growth by showing the 12-month change in jobs as a percentage, which allows for more direct comparisons between Kentucky and the U.S. and removes the seasonality of month-to-month changes.

Hiring vs. Separations

The “slow hire/slow fire” job market continues.

- Slow hire: Hiring in both Kentucky and the U.S. has deteriorated slowly. While the hiring rate in Kentucky was higher throughout much of 2025, it began falling in May 2025. Hiring in Kentucky has been lower than in the U.S. for 3 of the past 4 months.

- Slow fire: Layoffs and discharges held steady before increasing slightly with more recent months’ estimates. Firms appear less willing to hire, but also reluctant to make any major changes. Some call this a slow hire/slow fire job market.

- Layoffs in the news: Media stories of mass layoff announcements usually provoke more concern than is warranted. BLS data suggest there are around 1.7 million layoffs and discharges every month in the US. That said, recent preliminary estimates show a small increase in layoffs.

- Slow quit too: Quits have been low, suggesting workers aren’t finding (or expecting to find) better jobs than what they have.

Inflation

The Federal Reserve’s preferred inflation measure remains elevated.

- Core PCE & the Fed: Core Personal Consumption Expenditures (PCE) – which excludes food and energy – is the Federal Reserve’s preferred inflation metric. The Fed targets 2% inflation, which the US has not seen since 2021. Food and energy are excluded because they tend to be more volatile.

- Current rates: Inflation in March 2026 was 0.5 percentage points higher than a year ago. The increase in inflation shown since April 2025 is consistent with the effects of tariffs.

- Iran's impact on inflation: The spike in energy prices due to the war in the Middle East will be felt by consumers and businesses more quickly than they show up in core PCE, which excludes food and energy prices. Indirect effects will show up in various ways, such as higher shipping costs. Other inflation measures are already picking up these impacts. Read more about this below.

Other Measures of Inflation

Other inflation measures reveal the early impacts of war in the Middle East.

- Early indicators: The impacts of rising energy prices are already showing up in other measurements of inflation. The headline Consumer Price Index, or CPI, for example, ticked up to 3.8 percent in April 2026. Headline CPI includes food and energy and is a simpler inflation measure than PCE, meaning that it is produced with a smaller lag. Another measure, called the Producer Price Index – Final Demand, which shows what businesses are charging consumers for goods and services, also increased in March.

- What to expect: A measure of what businesses are paying for goods suggests that consumers may expect higher prices in the coming months. As seen on the chart above, the Producer Price Index – Intermediate Demand surged in March. This measure reflects the prices that businesses are paying for goods they purchase as inputs before selling to consumers.

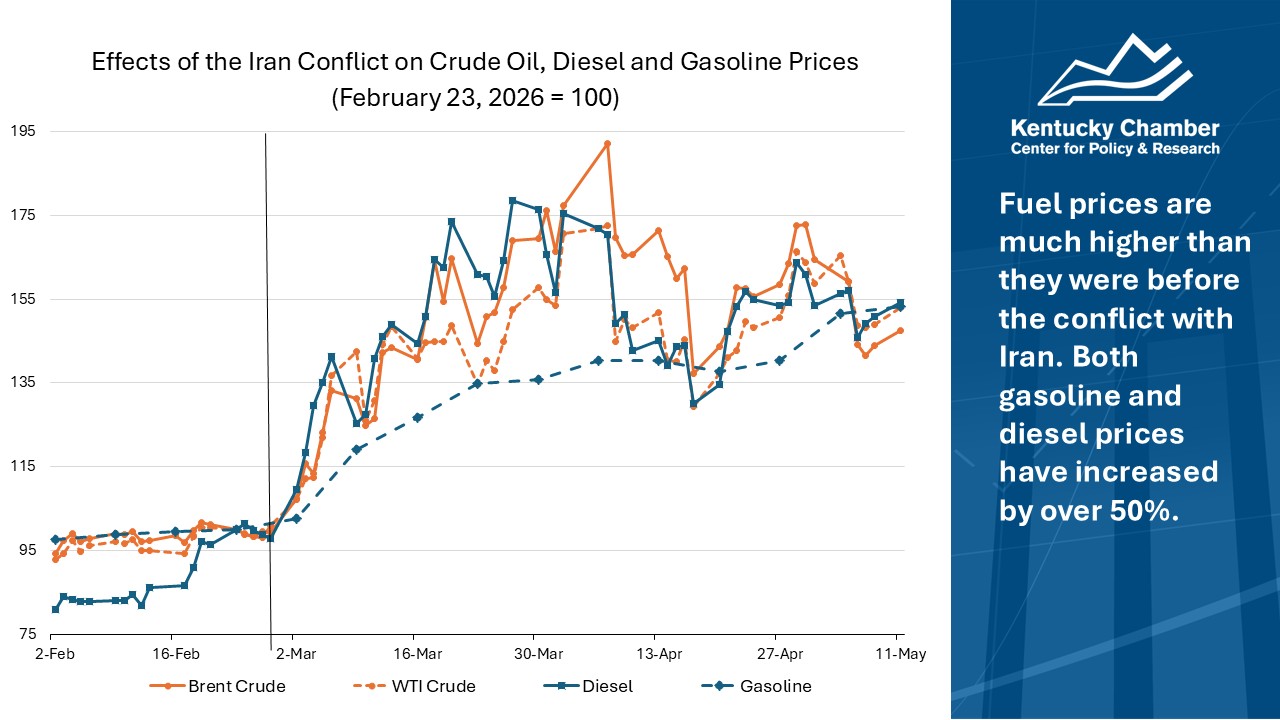

Energy Prices

Energy prices rose sharply after the conflict with Iran began.

- Indexing energy prices: This chart indexes prices for diesel, gasoline, West Texas Intermediate Crude oil (the standard benchmark for U.S. produced oil prices), and the international traded Brent Crude oil (the standard global benchmark) to February 23, 2026, just before the conflict with Iran started.

- Oil Prices: Crude oil prices continue to be 45-55% higher than before the conflict, despite the US and China both drawing down inventories.

- Gasoline and Diesel Prices: Gasoline prices tracked are “US Regular All Formulations Gas Price” as tracked by the U.S. Energy Information Administration. AAA tracks gas prices by formulation. As of 5/18/2026, the national average price for a gallon of regular gas was $4.515, compared to $3.179 one year ago. In Kentucky, regular was $4.166 compared to $2.878 one year ago.

- Impacts: Diesel prices will have greater impacts on costs to businesses due to how they influence shipping expenses, while gasoline prices will disproportionately affect everyday households.

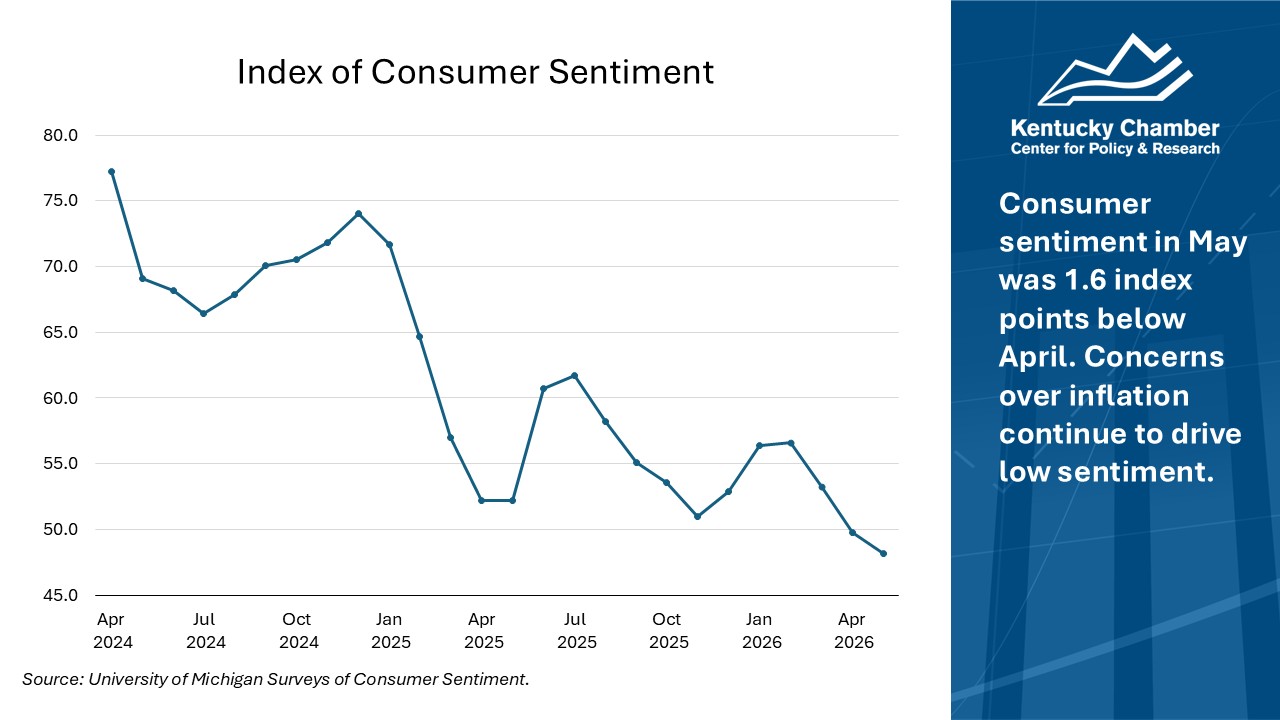

Consumer Sentiment

Consumer sentiment reached a new all-time low in May (after a new record in April).

- Consumer Sentiment: The University of Michigan produces an index of consumer sentiment and updates it monthly.

- All-time low last November: The November 2025 reading of 51.0 was an all-time low on the index.

- A new all-time low in May: The preliminary estimate for May, 48.2, is 8% lower than a year ago, and 16% lower than it was in February. Inflation concerns related to the conflict with Iran continue to play an important, negative role.

About This Data

On this web page, we provide economic updates on Kentucky and the United States, using a range of key metrics from the U.S. Department of Labor, U.S. Bureau of Economic Analysis, the University of Michigan, the St. Louis Federal Reserve, and the U.S. Chamber of Commerce. All data is analyzed by the Kentucky Chamber Center for Policy and Research. On this page, we cover jobs, unemployment, unemployment insurance claims, hiring, workforce participation, inflation, consumer sentiment, and small business optimism.

Sources

Federal Reserve Bank of St. Louis, Federal Reserve Economic Data

MetLife and U.S. Chamber of Commerce, Small Business Index

University of Michigan, Survey Research Center, Surveys of Consumers

U.S. Bureau of Economic Analysis, Personal Consumption Expenditures Price Index

U.S. Bureau of Labor Statistics, Local Area Unemployment Statistics

U.S. Bureau of Labor Statistics, Labor Force Statistics from the Current Population Survey

U.S. Department of Labor, Employment and Training Administration, Unemployment Insurance Data

U.S. Federal Reserve, Economy at a Glance – Inflation (PCE)

ADP Employment Report

Carlyle

Revelio Labs

U.S. Tariffs on Track to Hit 84-Year High Under Current Proposals, Tax Foundation Says

The Kentucky Chamber hosted a webinar on June 9, 2025, featuring Vice President of Policy Charles Aull and Erica York, Vice President of Federal Tax Policy at the Tax Foundation, to explore how tariff and tax policies in Washington are shaping the economic landscape for Kentucky businesses.

Watch the webinar below: